Update On Trump's Tariff Gambit

/It was back at the beginning of February that President Trump launched what I have called his “tariff gambit” — sequential edicts of flat-rate, economy-wide tariffs imposed against various of our trading partner countries. The process began with February 1 announcements of blanket 10% tariffs on all goods from China, and 25% tariffs on all goods from Mexico and Canada. Since then, in a blizzard of activity, there have been multiple rounds of announcements on this subject: new countries added to the tariff edicts, increases or decreases in the blanket rates applicable to various countries or products, granting of exceptions and exemptions, postponements of announced effective dates, and more. It’s more than just about anybody can keep track of. Here is an April 10 chronology from PBS compiling all the various tariff actions issued by the administration up to that time. The sheer speed of the announcements, and lack of direction toward any discernible purpose, are astonishing.

In a post about a month ago on April 8, I expressed extreme skepticism about this gambit. Perhaps, I thought, there could be an underlying intent to use these tariffs as leverage toward a regime closer to universal free trade than what we have previously had. But, I said, “that is not the stated rationale of the endeavor, and indeed it contradicts the stated rationale.” Moreover, I said, “if free trade is the end game, it needs to be accomplished quickly.” Tariffs that get entrenched for any period of time develop powerful constituencies and can be near impossible to get rid of.

Here we are a month later. Time for an update.

First, there has been no new trade deal yet announced with any country. Treasury Secretary Scott Bessent appeared to testify yesterday (May 6) before the House Appropriations Committee. Reuters has a report here. According to Reuters, Bessent said that the U.S. was negotiating with some 17 major trading partners, with some significant progress being made toward reducing trade barriers. Note that these are apparently 17 separate bi-lateral reciprocal trade negotiations, as opposed to a grand deal with all 17 together.

Here is a quote from Bessent:

"I expect that we can see a substantial reduction of the tariffs that we are being charged, as well as non-tariff barriers, currency manipulation and subsidies, both labor and capital investment," [Bessent] told the House Appropriations Committee.

That sounds encouraging. But then there’s this:

Bessent said about 97% or 98% of the U.S. trade deficit was with about 15 countries, most of which were major trading partners, and discussions were proceeding well with many.

Does Bessent (or for that matter, Trump) really believe that reducing trade barriers is going to have any significant impact on the “trade deficit”? I can’t think of any reason why it would. The “trade deficit,” otherwise known as the investment surplus, fundamentally represents the desire of people outside the U.S. to hold U.S. assets, particularly currency and government bonds, over other assets that they could potentially hold. There is no reason why that desire should decrease significantly if trade barriers are reduced. That desire could well even increase in an environment of freer trade.

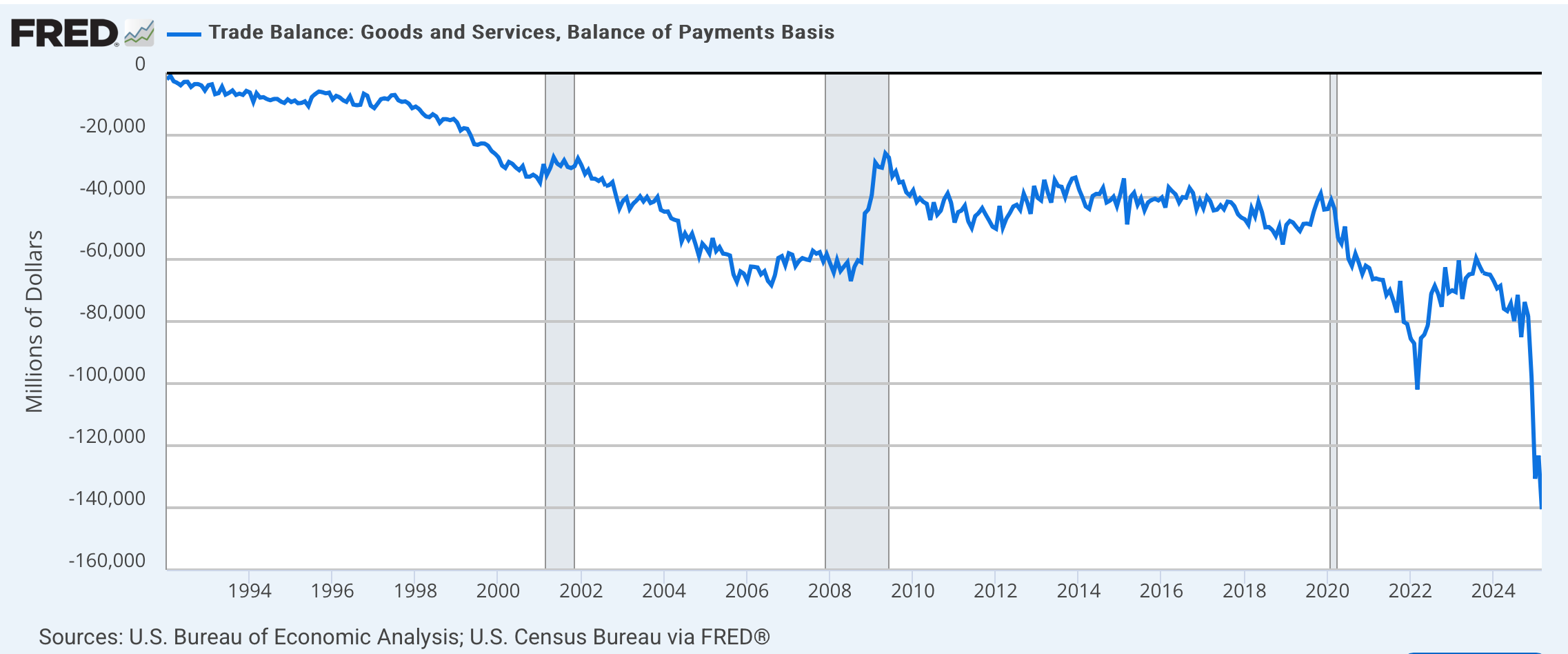

But meanwhile, if the goal of this tariff gambit is to reduce the trade deficit, so far the result has been rather a disaster. The Federal Reserve Bank of St. Louis puts out monthly figures for the trade deficit, compiled into a helpful chart going back to 1992. Their chart at the link has some cool inter-active features that don’t come over here in a screenshot, but here is the static version:

The three largest months for trade deficit, by far, have been the three months since Trump took office, with the most recent month reported, March 2025, setting a new record of over $140 billion. That compares to the previous all-time worst month of March 2022, at about $102 billion, which itself was an aberration. These last three months of extreme deficits could in part result from buyers of foreign goods rushing to stock up before the tariffs take effect; but there could be other causes as well. If you look at the chart, you will see that the best possible thing for reducing the trade deficit, if that’s what you want to do, is to have a good deep recession like we had back in 2008-09, when the deficit went down from about $60 billion per month to under $30 billion per month for several months. That reduction did not represent a time of prosperity or of “bringing the jobs back.”

At the Civitas Institute site, Richard Epstein has a post from April 30 explaining why sequential bi-lateral negotiations with separate countries are an unlikely way to achieve serious benefits to the U.S. from the international trade system. The title is “Why Reciprocal Trade Negotiations Will Fail.” The fundamental problem is that most international trade today is not just bi-lateral exchange between pairs of countries. Rather, most trade involves complex supply chains running through multiple countries. Epstein’s piece is typically dense, but here is an excerpt:

[T]he high trade deficits from asymmetrical dealings are still associated with high gains for both parties to the transaction. The deficits are a side effect of no economic consequence once we put these transactions in a wider global context. Thus, S [a seller] must acquire his inputs from somewhere [but not necessarily from the country that buys the product]. Commonly, the critical supply chains to which Trump refers occur across multiple countries, which means that the focus on reciprocal transactions is misplaced.

Epstein concludes that Trump’s bi-lateral approach “is doomed,” and he should “quit while he is behind” and go back to the flawed but far preferable World Trade Organization approach.

The question of how to deal with China is, I think, separate. There, questions of national security come into play. I don’t know that Trump’s approach to China makes sense either, but at least there is a rationale that makes sense.